6:36

Course Introduction - Time Series Modelling and Forecasting with Applications in R

NPTEL IIT Bombay

28:12

Week 01: Lecture 01: Time series introduction

28:01

Week 01: Lecture 02: Examples of time series data

29:27

Week 01: Lecture 03: Stationarity in time series

28:37

Week 01: Lecture 04: Weak vs. strong stationarity

31:10

Week 01: Lecture 05: Practical session in R - 1

28:27

Week 02: Lecture 06: Time Series Decomposition

28:56

Week 02: Lecture 07: Basic Time Series Processes

30:37

Week 02: Lecture 08: Autocorrelation and the Partial Autocorrelation Functions

28:09

Week 02: Lecture 09: ACF and PACF for Some Time Series Processes

30:43

Week 02: Lecture 10: Practical Session in R-2

31:51

Week 03: Lecture 11: Non-Stationary Time Series

29:53

Week 03: Lecture 12: Seasonality and its Features

30:41

Week 03: Lecture 13: Cyclicality and Test for Stationarity

26:33

Week 03: Lecture 14: Seasonality and SARIMA Model

31:52

Week 03: Lecture 15: Practical Session in R-3

Week 04: Lecture 16: Model Identification

31:16

Week 04: Lecture 17: Model Estimation

32:15

Week 04: Lecture 18: Diagnostic Checking -1

31:43

Week 04: Lecture 19: Diagnostic Checking -2

30:57

Week 04: Lecture 20: Practical Session in R-4

29:45

Week 05: Lecture 21: Forecasting Basics

30:23

Week 05: Lecture 22: Measuring Forecast Accuracy

29:03

Week 05: Lecture 23: Smoothing Techniques (SMA,EMA)

29:51

Week 05: Lecture 24: Double and Triple Exponential Smoothing

31:19

Week 05: Lecture 25: Practical Session in R-5

30:30

Week 06: Lecture 26: Persistent and Long- Memory Processes : Examples and Implications

29:20

Week 06: Lecture 27: ARFIMA Processes

29:32

Week 06: Lecture 28: Hurst Exponent - Estimation under ARFIMA

30:05

Week 06: Lecture 29: Estimation under ARFIMA

31:29

Week 06: Lecture 30: Practical Session in R-6

28:42

Week 07: Lecture 31: Multivariate Time Series Analysis: Examples and Motivation

29:41

Week 07: Lecture 32: Cross-covariance and Cross-correlation

29:40

Week 07: Lecture 33: Some Specific Multivariate Time Series Models

Week 07: Lecture 34: Further Extensions and Use Cases

28:55

Week 07: Lecture 35: Practical Session in R - 7

Week 08: Lecture 36: Cointegration and Further

29:12

Week 08: Lecture 37: Error Correction Models

27:41

Week 08: Lecture 38: Tests for Cointegration

28:49

Week 08: Lecture 39: Testing for Causality

Week 08: Lecture 40: Practical Session in R - 8

26:48

Week 09: Lecture 41: Frequency Domain Analysis

28:30

Week 09: Lecture 42: Spectral Representation of a Series

28:40

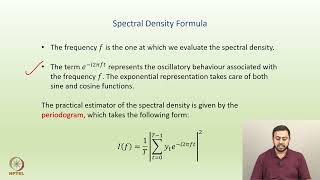

Week 09: Lecture 43: Spectral Density Estimation

29:14

Week 09: Lecture 44: Numerical Examples and Further

28:20

Week 09: Lecture 45: Practical Session in R - 9

26:54

Week 10: Lecture 46: Stochastic Volatility Modelling

Week 10: Lecture 47: ARCH Models

27:32

Week 10: Lecture 48: ARCH LM Test and GARCH Models

28:34

Week 10: Lecture 49: GARCH Model Extensions

28:36

Week 10: Lecture 50: Practical Session in R - 10

Week 11: Lecture 51: Nonlinear Time Series Models

27:18

Week 11: Lecture 52: Regimes and Nonlinear Models

Week 11: Lecture 53: Nonlinear Model Extensions

27:27

Week 11: Lecture 54: Markov Switching Models

27:58

Week 11: Lecture 55: Practical Session in R - 11

27:04

Week 12: Lecture 56: Machine Learning in Time Series

29:38

Week 12: Lecture 57: Linear Regression for Time Series and Beyond

28:17

Week 12: Lecture 58: Other Machine Learning Models for Time Series

Week 12: Lecture 59: Neural Networks for Time Series

29:25

Week 12: Lecture 60: Practical Session in R - 12